Finternet: A deep dive into a new financial system for the future.

Finternet: The internet’s cool cousin where financial systems mingle and collaborate in one big, interconnected network.

The fusion of finance and the internet, often dubbed “finternet,” is revolutionizing how we manage, invest, and think about money. This digital transformation is reshaping traditional financial services, democratizing access to financial tools, and creating new opportunities for both consumers and businesses.

As technology continues to advance at a rapid pace, the finternet ecosystem is expanding to encompass everything from mobile banking and peer-to-peer payments to robo-advisors and blockchain-based cryptocurrencies.

Let’s face it, managing money used to be a real drag. Remember the days of waiting in long lines at the bank just to deposit a check? Or trying to split a restaurant bill without a calculator? Well, those days are long gone, thanks to the finternet revolution. Now, we’ve got a whole world of financial tools right at our fingertips!

The Convenience of Mobile Banking

Remember the days of waiting in long lines at the bank? Those days are history! Mobile banking has changed the game:

- Check your balance anytime, anywhere

- Pay bills with a few taps

- Transfer money to friends instantly

- Deposit checks by simply taking a photo

Investing Made Easy

The world of investing isn’t just for Wall Street pros anymore. Finternet has democratized investing:

- Investment apps allow you to start with small amounts

- Robo-advisors provide personalized advice at a fraction of the cost

- Real-time market data at your fingertips

- Fractional shares make expensive stocks accessible to everyone

The Crypto Revolution

Love it or hate it, cryptocurrency is shaking up the financial world:

- Decentralized currencies like Bitcoin challenge traditional banking

- Blockchain technology offers new levels of security and transparency

- NFTs are changing how we think about digital ownership

- DeFi (Decentralized Finance) platforms offer new financial services

Blockchain and Finternet: The Solana Revolution

When it comes to blockchain powering the finternet, Solana is leading the charge. This high-performance blockchain is designed to make decentralized finance (DeFi) accessible and practical for everyday use:

- Lightning-fast transactions: Solana can process up to 65,000 transactions per second, making it perfect for real-time financial applications.

- Minimal fees: With transaction costs often less than $0.01, Solana makes micro-transactions viable.

- Smart contract capabilities: Developers can build complex financial applications on Solana, from decentralized exchanges to lending platforms.

- Interoperability: Solana’s wormhole protocol allows for seamless asset transfers between different blockchain networks.

Solana’s ecosystem is rapidly expanding, with projects like Serum (a decentralized exchange) and Pyth Network (a real-time financial data oracle) showcasing its potential. As finternet continues to evolve, Solana’s scalability and efficiency position it as a key player in bridging traditional finance with the decentralized future.

What is the need of Finternet?

The Financial System’s Outdated Infrastructure

Today’s financial system is like an old machine trying to keep up with modern demands. It’s struggling in three key areas: speed, cost, and accessibility. Let’s break these down:

Slow as Molasses

While we can send messages across the globe in seconds, our money often moves at a snail’s pace. Why?

- Outdated Systems: Many financial transactions still rely on old-fashioned databases and messaging systems that don’t play well together.

- Physical Paperwork: Believe it or not, some transactions still require actual paper documents.

- Time Zone Troubles: Cross-border transactions can get stuck waiting for business hours in different parts of the world.

- Regulatory Red Tape: Important anti-crime checks often involve repetitive, manual processes that slow things down.

Costly Complications

Slow finances aren’t just frustrating — they’re expensive. Here’s how:

- Cash Flow Crunch: Delays tie up working capital, forcing businesses to keep large cash reserves or resort to pricey credit options.

- Waiting Game Woes: When paychecks or government aid are delayed, people might turn to high-interest loans to get by.

- Risk Management Expenses: To guard against potential transaction failures, financial institutions require costly collateral.

- Error-Prone Processes: Manual systems lead to mistakes, requiring extensive (and expensive) auditing and back-office work.

- Lack of Competition: With few alternatives, some financial services charge sky-high fees, especially for small or international transactions.

Limited Access and Options

The combination of sluggish systems and high costs creates a domino effect:

- Service Deserts: Some areas, especially rural or low-income regions, lack basic financial services because they’re deemed unprofitable.

- Shrinking Networks: Cross-border banking relationships have been declining, further limiting options.

- Suboptimal Choices: People often settle for low-interest savings accounts or expensive credit cards due to lack of alternatives.

- Innovation Roadblocks: The current system makes it difficult to implement potentially game-changing ideas like smart contracts for trade finance.

- Exclusion: A staggering 1.4 billion adults worldwide still lack access to basic financial services.

By breaking down these issues, we can see how the current financial system’s shortcomings create a ripple effect of inefficiency and inequality across the global economy.

What’s Next for Finternet?

The future of finance is looking more exciting than ever:

- AI-powered personal finance assistants

- Increased integration of augmented reality in banking apps

- Biometric security measures for safer transactions

- Green fintech focusing on sustainable and ethical investing

As we dive deeper into this Finternet era, it’s clear that managing our money will never be the same. And you know what? That’s something worth getting excited about!

User-Centric Finance: The UPI Revolution

Finternet has put users at the center of the finance ecosystem, and nothing exemplifies this better than India’s Unified Payments Interface (UPI):

- Instant, 24/7 money transfers between bank accounts

- Simple mobile interface accessible to everyone with a smartphone

- QR code payments making transactions a breeze for small businesses

- Open architecture allowing for innovation and competition

UPI’s success shows how user-centric design can transform an entire nation’s payment landscape.

Unifying Countries Through Fintech

Finternet isn’t just changing how we handle money within borders — it’s reshaping international finance:

- Cross-border payment apps reducing fees and wait times

- Digital remittance services helping migrant workers support families back home

- Blockchain-based systems creating a universal financial language

- Fintech sandboxes allowing countries to collaborate on regulations

These developments are slowly but surely creating a more unified global financial system.

The Multi-Faceted World of Tokens

In the finternet era, tokens are more than just digital money. They can serve various functions:

- Currency tokens: For buying goods and services (like Bitcoin)

- Utility tokens: Granting access to specific services (like Filecoin for storage)

- Security tokens: Representing ownership in assets (like tokenized real estate)

- Governance tokens: Giving voting rights in decentralized organizations

This versatility allows for creative solutions to complex financial problems.

Four Types of Digital Assets

The finternet landscape includes four main types of digital assets, each playing a crucial role:

- User-controlled assets: Like cryptocurrencies, fully owned and managed by users

- Attested assets: Digital representations of physical assets (e.g., tokenized gold)

- Registered assets: Legally recognized digital assets (e.g., security tokens)

- Regulated assets: Digital versions of traditional financial instruments (e.g., CBDCs)

These asset types form a spectrum from fully decentralized to highly regulated, allowing the finternet to bridge traditional and cutting-edge finance.

By leveraging these concepts, finternet is creating a more inclusive, efficient, and innovative financial world. Whether it’s making daily transactions smoother through UPI, facilitating global money movement, or introducing new forms of assets and ownership, the finternet revolution is reshaping our relationship with money at every level.

From Digitization to Tokenization: The Evolution of Assets

Let’s break down how we’re moving beyond just making things digital to creating a whole new world of possibilities:

- Digitization: The Basic Upload Remember when we started scanning documents instead of keeping paper files? That’s digitization. It’s like taking a photo of your stuff and storing it on a computer. It’s great for keeping things organized, but it’s mostly for internal use. Sharing these digital copies between different companies? Not always easy.

- Dematerialization: Saying Goodbye to Physical This is when we decided we don’t need the physical thing at all. Think about how you used to get stock certificates, but now it’s all electronic. Your ownership is recognized without needing any paper proof. It’s legally valid too!

- Tokenization: The Smart Digital Asset Now, this is where things get exciting! Tokenization takes those digital assets and makes them super smart and flexible. It’s like giving your digital assets superpowers:

- They can move around easily, like sending a text message

- Anyone can access them, not just big players

- They’re affordable because they’re so easy to manage

- Each token can do things on its own, without needing a middleman

- You can program them to behave in certain ways automatically

Imagine if your house could automatically pay its own property taxes, or if your car could rent itself out when you’re not using it. That’s the kind of stuff tokenization makes possible!

The Innovation Playground

With tokenization, we’re creating a world where new ideas can thrive:

- Costs are low, so more people can participate

- Trust is high because everything’s transparent and secure

- Things move fast — no more waiting days for transactions

- New business ideas can be tested quickly and easily

It’s like we’re building a giant sandbox where anyone can come play and create new things. This could lead to a future where:

- Starting a business is as easy as setting up a social media profile

- Investing in real estate could be done with pocket change

- Global trade happens instantly, without currency exchange headaches

- Your digital identity could manage all your assets automatically

By making assets smarter and more accessible, we’re not just changing how we handle money and property — we’re opening up a whole new world of possibilities for everyone. And that’s what the finternet revolution is all about: creating a fairer, faster, and more innovative financial world for all of us.

Finternet and Public Ledgers: A Powerful Combination

While Finternet is revolutionizing how we interact with financial services, its combination with public ledgers is opening up even more possibilities. But first, let’s understand what public ledgers are:

What are Public Ledgers?

Public ledgers are decentralized, transparent, and immutable record-keeping systems. Unlike traditional ledgers managed by a single entity, public ledgers are maintained by a network of computers. The most well-known form of public ledger is blockchain technology.

Key features of public ledgers include:

- Transparency: All transactions are visible to anyone in the network.

- Immutability: Once recorded, transactions cannot be altered or deleted.

- Decentralization: No single entity controls the ledger, increasing security and trust.

- Consensus mechanisms: Ensure agreement on the state of the ledger across the network.

Public ledgers form the backbone of cryptocurrencies like Bitcoin, but their potential extends far beyond digital currencies.

Now, let’s explore five key use cases where Finternet and public ledgers work together to create innovative solutions:

- Transparent Financial Transactions: Public ledgers enable complete transparency in financial transactions. Every transaction is recorded and can be verified by anyone, reducing the risk of fraud and increasing trust in the financial system. This transparency can help combat corruption and improve accountability in both private and public sectors.

- Decentralized Finance (DeFi) Applications: DeFi applications leverage public ledgers to create financial services without traditional intermediaries. These can include decentralized exchanges, lending platforms, and yield farming protocols. DeFi opens up financial services to anyone with an internet connection, potentially increasing financial inclusion globally.

- Cross-border Payments and Remittances: By using public ledgers, cross-border payments and remittances can become faster, cheaper, and more transparent. This can significantly benefit migrant workers sending money home, reducing fees and wait times associated with traditional remittance services.

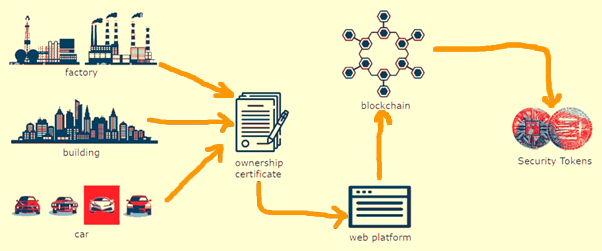

- Tokenization of Real-world Assets: Public ledgers enable the tokenization of real-world assets like real estate, art, or commodities. This allows for fractional ownership, increased liquidity of traditionally illiquid assets, and easier transfer of ownership. It could democratize access to high-value investments.

- Automated Compliance and Audit Trails: Public ledgers create immutable audit trails, making compliance and auditing processes more efficient and reliable. Smart contracts can automate many compliance procedures, reducing costs and the potential for human error in regulatory reporting.

These use cases demonstrate the transformative potential of combining Finternet’s connectivity with the transparency and immutability of public ledgers. As these technologies continue to evolve and integrate, we can expect to see even more innovative solutions that address long-standing challenges in the financial world.

The synergy between Finternet and public ledgers is creating a financial ecosystem that is more transparent, accessible, and efficient than ever before. It’s paving the way for a future where financial services are not just digitized, but fundamentally reimagined to serve a broader range of people and purposes.

This combination is not just changing how we conduct financial transactions; it’s reshaping the very nature of trust in financial systems. By leveraging the strengths of both Finternet and public ledgers, we’re moving towards a financial world that is more open, fair, and innovative for everyone.

The integration of public ledgers into Finternet applications addresses many of the challenges faced by traditional financial systems. It provides a level of transparency and security that was previously unattainable, while also enabling new forms of financial interaction and asset management. As this technology matures, we can expect to see a radical transformation in how we think about and interact with money and value in the digital age.

As we embrace this new era of finance, it’s crucial that we address challenges such as data privacy, cybersecurity, and financial literacy. Regulators, innovators, and users must work together to ensure that Finternet develops in a way that is not only technologically advanced but also ethical and inclusive.

In the end, Finternet is more than just a set of technologies — it’s a paradigm shift in how we think about and interact with money. It’s creating a financial world that’s more open, more efficient, and more equitable. As we stand on the brink of this new financial frontier, one thing is clear: the future of finance is here, and its name is Finternet.

References

- The Vision for the Future Financial System

- Finternet: technology vision and architecture

- Fireside Chat: The Financial System for the future

- All the respective links are hyperlinked in the texts itself.

If something is left by mistake please reach out :)